[ad_1]

Learning to reconcile with QuickBooks Online is a starting step for using QuickBooks to manage books. QuickBooks is a handy tool to help you reconcile your accounts without using any external tools.

In this article, we walk through the reconciliation process in QuickBooks, address common issues, and provide useful tips.

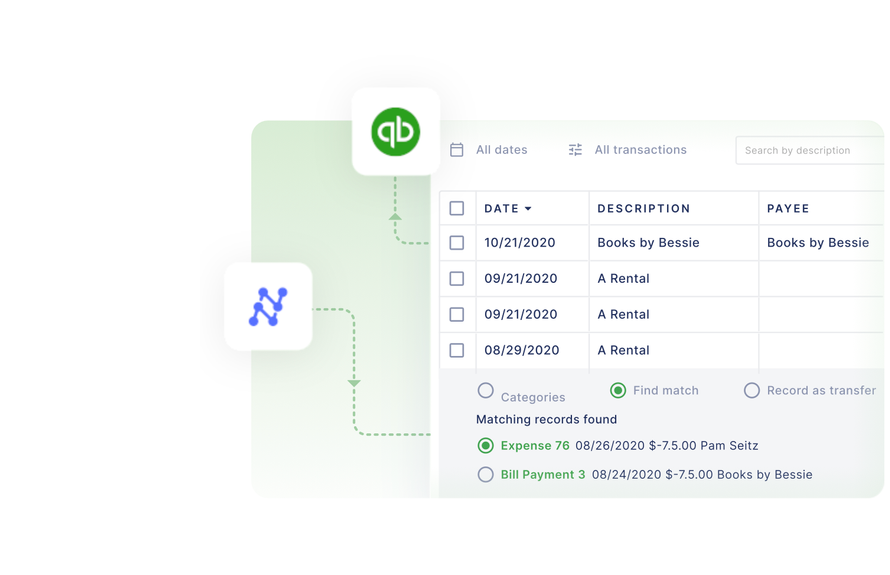

Search for “Reconcile” in the top help menu bar. Choose the account you want to reconcile.

Step 2: Reconciliation Opening Balance

The opening balance and date are automatically detected based on the ending balance and the date of the previous reconciliation.

If this is your first time reconciling in QuickBooks Online (QBO), the transactions will be listed from the beginning of the account and the opening balance will be zero.

If you wish to learn more about previous reconciliations, such as the statement end date, you can locate this information in the “History by account” section.

Step 3: Reconciliation Closing Balance

Enter the closing balance and ending date. You can also opt to add the “service charge” and “interest earned’ fields.

Service Charge: Input any service charge amounts imposed by your bank. Enter the data, amount, and the expense account. You can add an expense account like “Bank Service Charges.”

Interest earned: Fill the field to account for the interest earned from your bank. Enter the data, amount, and the expense account. You can add an expense account like “Interest Earned.”

Step 4: Match and Clear Transactions

The QBO reconciliation screen shows a tick mark and grey background for cleared transactions. While the unmatched transactions appear at the top.

For each unmatched transaction, find the matching transaction on your statement. If the amount matches, clear the transaction. Repeat this process till all the transactions are matched. If the difference hits 0, congratulations, your account is reconciled. Press “Finish Now” to complete the reconciliation.

If the difference is not zero, you must identify the transactions that aren’t recorded in QuickBooks. This can be due to accounting errors, unaccounted charges, or unauthorized transactions.

Identifying errors in your reconciliation

1. Outstanding Payments & Deposits

Due to banking delays, outstanding checks and deposits-in-transit aren’t recorded in the bank statement or can be recorded after the closing date. This can be unaccounted for in your bank statement.

2. Accounting Entry Error:

Transaction amounts or dates can be incorrectly entered. This can lead to a number mismatch, leading to unmatched transactions.

3. Bank Charges or Interest Earned:

If you haven’t accounted for this at the start, this can lead to your bank balance reflecting a different amount.

4. Unauthorized transactions, fraud or theft

Companies worldwide lose up to 5% of their revenue to fraud and theft. This could be due to unauthorized employee transactions or theft of credit card or bank account credentials. Reconciliation is a really helpful process to identify this and quickly report it to safeguard the company from losses.

Automate Bank Statement Reconciliation

Reconciling with QBO requires a lot of manual effort and can be time-consuming. This is a bigger problem with companies with high volume and quick turnaround times. Reconciling 100s of transactions can take days to resolve completely.

You can reduce the reconciliation process to minutes using automation software. This would require aggregating data from multiple financial sources, extracting relevant data from documents, matching data across different sources, and fraud checks.

If you are looking to automate your bank reconciliation process, set up a demo call with our experts to automate your workflows using Nanonets.

Automate fraud detection, bank reconciliations or accounting processes with a ready-to-use custom workflow.

Reconciliation software can automate 3 key items for you:

- Data collection – Automation software like Nanonets can seamlessly integrate with your ERP or Email to gather documents like cashbooks, bank statements, invoices, and receipts. The software will only pull relevant information from each document through OCR technology.

statements - Data matching – With no code automation, you can easily set up rules to match the two documents. You can set up new rules with time & don’t have to struggle with formulas.

- Identifying error & fraud-check – Setup flags to identify any irregular transactions, duplicates, or unauthorized transactions.

[ad_2]

Source link